Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv U.S. Senate CSPAN January 17, 2013 9:00am-12:00pm EST

9:00 am

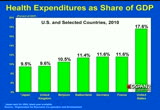

let's take the savings that the speaker was proposing on health care, he said 500 billion over 10 years. again, if we put that in context, we're going to spend over $11 trillion on health care. so the spending proposal that the speaker made represents 4.5% of health care spending over the next 10 years. we can't say for%? really? what company in american face with the circumstance that we have would say oh, no, that's too tough, we can't save 4%. yes weekend. let's go to the next slide. you know, especially if you put in contest where we are with health care expenditures in the world, the most recent year for which we have comparisons with other countries was 2010. we know that we are now over 18% of gdp on health care in this country.

9:01 am

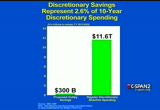

nobody else is more than 11.5. so the idea that we can't have additional savings and health care and not hurt anybody is preposterous. we absolutely can have savings in health care. and by the way, when you savings in health care, 40% of the savings flows through the federal government and federal programs. because federal government is funding 40% of the health care in this country. so we have big savings in health care. we have big savings for the federal government. discretionary savings, the speaker proposed 300 billion over 10 years. again, if we put that in context are going to spend $11.6 trillion over the next 10 years. so that would represent a savings of 2.6%. as judd indicated we've already had and the budget control act 900 billion of savings, so there are substantial savings that have already occurred in this

9:02 am

area. but we can do another 300 billion. we could save another 2.6%. other mandatory, that's the other major category. again, speaker proposed $200 billion over 10 years. we are going to spend $11 trillion -- i'm sorry, $511 trillion in this category over the next 10 years. so that represents a 10 a savings of 4%. you know, what have we become as a country if we can't make a 4% change? really, that is something we should be able to do. so under the compromise that i proposed, taking the speakers numbers, taking the president's revenue, you can see how it racks up to a total of over $4 trillion of savings over 10 years, which is, as i indicated, what virtually every economist

9:03 am

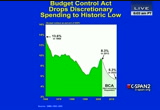

says is necessary to get us back on track. now, we are borrowing 31 cents of every dollar we spend, but we are also on a long-term path, judd knows so well, according to the congressional budget office, if we failed to act we are headed for a debt that will be 100% of our gdp, it will be 200% of our gdp. so there is incredible and to act here. not just together and delay and awful, but to act. the budget control act has already dropped discretionary spending to historic lows. you can see under the budget control act we're going to go down to 523% of gdp going to discretionary spending, down from 8.3% last year. 13.6%. we are already have made very substantial changes on the

9:04 am

discretion side of the house. where we really need to focus these health care -- judd make this point -- medicaid, medicare, other federal health spending as a percentage of gdp. going back to 1972, looking forward to 2050, you can see 1972 we were spending 1% of our gdp on these health care accounts. we are headed on the current trendline to spend 12% of our gdp on these accounts. so this is the 800-pound gorilla. this is the problem that we've got to confront. social security is pretty stable as a share of gdp. gone up a little bit, a global more with the baby boom generation. that's not the problem. here is the problem. if you look at the fiscal commission plan, where judd and i served, it had, if you look at current comparisons, over

9:05 am

$5 trillion of deficit reduction. lowered the deficit to 1.4% of gdp in 2022, stabilize the debt by 2015. it even further reduced discretionary spending. it builds on health reform savings and called for social security reform, and provided specific things to do to get social security solvent for the next 75 years here and also include fundamental tax reform that raise revenue. and raised quite a bit of revenue, 2.4 trillion of that 5.4 trillion would have been revenue, but revenue not required raising rates, but revenue that would come through reforming the tax code, reducing preferences, exclusions that are shot through the tax code, to actually be able to reduce rates

9:06 am

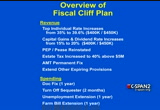

and raise additional revenue. for anybody that wanted can you really do that, remember tax expenditures are running $1.2 trillion a year. we are spending more for the tax code than we are through all of the appropriate accounts of the federal government. this is what happens to the deficit in the share of gdp under the fiscal commission plan. you can see a dramatic improvement. the fiscal cliff plan, and what was just adopted, you all know the elements here, individual rates were raised, capital gains and dividend rates were raised, the estate tax was increased to 40% above $5 million. alternative minimum tax was six on a permanent basis paper extended other expiring tax provisions. on the spending side, a doc fix was taken care for a year.

9:07 am

we turn off the sequestered for two months. the unemployment extension was included for a year, and the farm bill was extended for a year. but don't let anybody tell you that had anything to do with deficit reduction. because here's what congressional budget office said. said the total revenue lost from the proposal is $3.6 trillion. that is from extending all the bush-era tax cuts except for the top 1%, and the permanent fix to the alternative minimum tax, those two things lose 3.6 trillion of revenue. additional spending, 332 billion. so the deficit was increased by $4 trillion, and that doesn't count debt service. it would be another $650 billion. so we just dug the hole deeper. and anybody who tells you this thing raised net revenue over 10 years, no, we didn't. it absolutely did not.

9:08 am

because when you fix the alternative minimum tax for 10 years, that costs you $1.8 trillion. so you picked up 650 billion by raising the rates on the top 1%, but you have permanently fix the alternative minimum tax, which in the law was going to generate $1.8 trillion over this 10 years. what's bigger? 1.8 trillion or six under 50 billion? i'll tell you, republicans should have been celebrating this as a massive victory, a massive tax cut because, in fact, that's what has occurred here. this is a big tax cut. so i say to you in terms of what has to happen next, i think it's going to require the revenue side of the equation and the spending side of equation to be addressed. let me just conclude by saying this. how do we get out of this in the

9:09 am

current circumstance? the president said he's not going to negotiate on the debt limit. republicans say they will not vote for an extension of the debt limit unless they get substantial additional cuts in spending. i think judd is absolutely right. we have another dynamic at work here, and that is the sequestered. $1.2 trillion of across the board spending cuts, having defense, half in nondefense. republicans don't like it, democrats don't like it. that creates an opportunity. there's also the question of how long do you extend the debt limit. i think it would be incredibly foolish to renege on the debt of the united states. it would be enormous consequences. that is a losing proposition for everyone. but how long we extend the debt limit, that is open to negotiation. and between the two of how long you extend the debt limit, and number two, how you deal with

9:10 am

the sequestered, gives you an opportunity for another attempt at a grand bargain. revenue and spending we strength, especially on the mandatory programs to get america back on track. we can do. we done much tougher things before. and this is our next opportunity to put america in a preeminent position in the world. if we solve this problem, there is nothing that can stop the united states from continuing to be the most important and dominant country in the world. thank you. [applause] >> thank you very much. senators conrad, senator gregg. we're going to open it up to questions, but i'd like to start with one. we know what the problem is, and we sort of know how to solve it.

9:11 am

but we are confronted by the reality of the political dynamics on the hill, a republican house that was elected within their districts by large margins, and the president who won an election. how do we bridge the gap? how do we actually get the deal done? >> you know, we have a system that is incremental in nature. we are not a parliamentary system where if you control the government you can move very quickly and the pendulum swings aggressively. american politics has played on the 40-yard line and that's especially true during a time where you have a divided government. both sides feel very, very

9:12 am

strongly about their positions. but there is a deep identity of interest here that i think leads to agreement, or should lead to agreement. the identity interest is this. the president of the united states, there are two events which you know may occur in the next come in this next four years which could totally derailleur capacity of the of the things you want to do about the nation, your agenda. the first is that terrorists with a weapons of mass destruction. i think this president has been very aggressive in trying -- that issue and his commitment to intelligence gathering and his use of various capabilities to reduce that threat. and secondly, the issue of a financial crisis, driven by the markets and our currency because of the fact that they take a look at the charge that kent has put up there and they said hey, these people can't figure debt. that is going to happen if we

9:13 am

continue on his present course but at some point so wakeup, financial markets someday and say, these guys, the dollar is not with what they claim because they can't pay it back without inflating the dollar. you don't want to happen on your watch because it's only sidetracked economy. so the president has an incentive to come to the table and tried to get the issue under control. and you have the republicans issue which part of the republican dna, fiscal responsibility, balanced budgets, trying to get the deficit under control. most of the people have been elected in the last few years have been elected basically on the fiscal policy agenda coming out of a coming out of the tea party initiative. so that you have an identity of interest. the question really becomes the politics of getting people to go across the aisle to reach agreement. and i don't think the house can do it very honestly.

9:14 am

because the fact so many seats in house now are gerrymandered by party. and the one thing that happens in those districts, about 65% of the house is now gerrymandered by party, when you're elected your elected by the base. you win the primary you are the congressperson. the one thing you can't do with your base is compromised. that's the one thing the base won't tolerate, on both sides. you can't govern because govern requires compromise. you can't go across the aisle because you are threatened immediately on the reelection. so i think the house is sort of locked down unless it gets leadership. so i think leadership has to come from is the president. the president has to step into this issue and lead. he's got allies in the senate who are willing and capable of going across the. the senate has a very strong working center. one of the primary movers. it's almost half the senate is willing to move on a very big

9:15 am

and aggressive package if they get leadership. then you take the package that comes out of the senate, take it to the house with the presidential leaders -- leadership come and speaker boehner i think would be supportive, and to get something done. >> i really agree with that. in a curious way, both sides need each other. why do i say that? because the debt limit has to be extended. simply has to be. this is not our future spending. this is about spending that's already been done. the question here is are we going to pay the bills we have already racked up. clearly we have to do that. the consequences of our failure to extend the debt limit would be extraordinary. but to do that you've got to get votes of people in the house of representatives. and they are insisting on additional spending we strength. in fact, we need additional spending we strength. i think of anything is clear from the charts i put up here is

9:16 am

we have got to get some additional we strength on the entitlement side of our budget. and so it does lend itself to a compromise, one in which there is additional revenue, not from raising rates, but through tax reform, which happily is something the country needs anyway. does anybody believe this tax code that we've got makes any sense at all? i don't know of a single democrat or a single republican who would sit here and say this tax code can possibly be supported on any ground. it's not fair, it's not rational, it's not easy. to abide by. and it is hurting our competitive position in the world. solo, it just seems to me we have a continuing opportunity here to have a compromise. and one that would get us back on track.

9:17 am

it does require leadership. i've always believed it has to start in the senate because that's where there's been still a broad middle, to really believe that we need to have action. spinning i would like to open it up for questions from you all. so if you would raise your hand, and i think we have one right over here. and if you could please state your name and organization please. >> tony with bloomberg government. so both your comments as you just talking about seems to indicate that there's some positive momentum behind tax reform. is the on the individual site? is that on the corporate side, or is it on both? how do you handicap your prospects for that, say, in the next one or two years? to get something done. >> i think it's on both sides. as you know, our statutory rate is now the highest rate in the

9:18 am

world, in the industrialized world, in terms of corporate t tax. that's, our effective rate is substantially lower than that. we are in the mid-pack in terms of our effective rate. but, unfortunately, some companies pay pretty close to the statutory rate. clearly we need to change the corporate tax. that cries out for reform. the individual, you know, i just find it grossly unfair that some people who are making staggering amounts of money pay much less of a tax return the people who are working for them. so i think in the next couple of years you've got, even in the next year, you've got a substantial opportunity for tax reform on both sides and back i would agree with it. i think both chairman have made -- moving this way. i don't see how you get this deficit under control, and lets

9:19 am

you change the tax laws. i think what the template of simpson-bowles has to amazingly aggressive steps into. one was massive tax or form, which was excellent positive, short of being done. as kent other to do, eliminated $1.1 trillion of deductions annually, so we produce $1.1 trillion of revenue. we took a trillion of that, simpson-bowles rates were nine, 15, 23. and we took 100 billion, we reduced debt. and that's what template makes a lot of sense from a republican standpoint, there's great incentive because republicans want the rate down so people invest their return for purposes of tax avoidance. democratic side you've got guys like ron wyden and kent want to see them because they see these tax loopholes, these tax cuts as special interest. so there's identity of interest

9:20 am

here, plus both sides want simplification and want fairness. on the corporate side, i think it's critically -- i think one of the keys that has to be addressed here is the issue of a, some sort of territorial system. because we've got trillions of dollars sitting overseas in corporations who can't get it back here to the united states because have to pay 35% to recognize. you've got this foolish cbo scoring mechanism which says if you bring 1 dollar back into don't pay 35 cents attacks on, government loses 35 cents. well, the dollar never comes back. we are locked in this scoring mechanism problem coupled with the fact that these companies are looking overseas to buy companies and expand when they should be using those resources to expand here. there needs to be some sort of territorial system. i understand labor opposes this. because they think that the money, companies may move more people offshore because they will see lower taxes. i think that's just foolish.

9:21 am

i think, to bring that money back it means you're going to get better invest in your. you will get more expansion of capital and equipment here and more jobs here. and so some sort of territorial system. >> right here. >> i'm sheila with the national housing coalition. thanks to both senators are coming this morning and for your service. i have two questions. the first one is, can you talk about your sense of the potential for change to the mortgage interest deduction? the bowles-simpson plan would have modified the mortgage interest deduction. and, too, can you talk about why it is that raising the cap on social security tax really isn't part of the discussion? >> well, raising the cap on social security was part of bowles-simpson. we recommended that.

9:22 am

on mortgage interest, i think ultimately it will be changed. that there will be, you know, bowles-simpson talked about a credit which is a more efficient way of doing it than doing it as a deduction. and not allowing it on second homes and having a cap of 500,000. i don't think 500,000 would probably be adopted, but current is only but i think that will be reduced to i think second homes will be excluded to simply. as part of an overall package. now that's with an overall package, and as i've indicated i stood in hopeful that one will be done. it's so needed, and it's very hard for me to say i don't do this unless both sides walk together. democrats control the senate, have the white house. republicans control the house. i really believe there's a

9:23 am

possibility of getting this done. if it starts with the president and the senate, and then you give it to the house and let the pressure built. spent i look around this room and i don't see too many people who are here with reagan rostenkowski. the one thing that was necessary to accomplish -- first you have to have the president. the president has to be engaged to get tax reform. and secondly everybody else, you can't pick out one. you have to do everybody. and so i don't think there's any question but the four major sources of revenue, four major sources of elections which create revenue, will all have to be impacted and that includes real estate, charitable giving state and local and health insurance. because that's where all the deductions occurred.

9:24 am

>> as congress looks at, you know, cutting expenditures, raising revenue, how will its five -- health care expenses, versus retirement savings which arguably are more of a long-term hit to the economy, and if people who look to fund their retirement? >> let me just say, we've got to be smart about this. and i don't think we should do things that would this incentive savings and investment. that's one of the bizarre things about the current tax code. the incentives are really all wrong, if you think about the i

9:25 am

say this as a democrat. i mean, if you don't have savings you don't have investment. if you don't have investment, you don't grow. but our current incentives with this tax code are all upside down. so we disincentive because we tax. we should not do that with respect to helping people build for their own retirement. and that means they need to be in savings vehicles, social security is certainly one. but they also need to be in other tax preference savings vehicles. i don't think it would be smart to hurt those. spent i certainly agree with that but i think there is a bigger matter and that's the policy of the fed, because

9:26 am

you're basically creating a situation because of the lower interest policies where seniors savings are being disincentivized in a very aggressive way. and i understand the policies they are pursuing but they have a disproportionate impact on the savings. >> we have time for one more question. and some quick answers. go ahead. >> thank you, good morning. peter from the american association of advertising agency. thank you both for your remarks today. it's been very interesting. another discussion that's occurred among some economists is that it's a question the fundamental assumptions of what you describe here but rather a question of timing, that the focus should be more about stimulate the economy, getting folks back up and working and then having that discussion about the deficit. because, in fact, the credit is relatively easy, the dollar is still the de facto currency standard. as many positions of strength to leverage right now to move

9:27 am

forward. if i could just have your thoughts on that and then quickly, would you think corporate tax reform discussion will go within the next six months? thank you. >> always, there's always an excuse for not doing things in washington. and welcomed you don't want to retire -- the simple fact is the best thing you do for this economy is resolve our long-term fiscal problem. because it would give people confidence in our future. it would cause people to go out and be willing to invest and it would say to our kids, you're going to have a prosperous lifestyle first have to pay for our generation. and so i just don't accept this argument. sure there's some short-term things that would contract spending but that's not going to happen anyway. i mean, i just don't see that happening. so i just think that the sooner we get on this issue of resolve our long-term fiscal problems, the more dynamic our economy

9:28 am

will be because we have done that. >> let me just say, i am in the camp that believes when the major problem of economy is facing is weak demand. that is not the time to impose fiscal austerity. but it is the time to put in place a plan that gets us back on fiscal track over the longer-term. that is precisely what bowles-simpson's -- bowles-simpson attempted to do because we did not impose austerity immediately. we had a several year gap. but put in place, the long-term changes that gave you an assurance that you are going to get back on track over the ten-year budget period. so to me there is a matter of timing you. i think you want to be very wary of imposing austerity to quickly on an economy that is still recovering. and after all, we've just had the toughest economic downturn

9:29 am

since the great depression. so i think we do have to be sensitive to what you do in the short term. but that is no excuse for taking action that gets us back on track long-term. the happy part about this is the tax changes and spending changes that you need to make have enormous benefit, not only in the ten-year budget window, even if you give several years delay to allow the economy to recover, but the real big bonus is what greg was talking to, senator gregg was talking about earlier, the second 10 years and the third 10 years. if you make these fundamental changes now, they pay massive dividends off into the future. [inaudible] >> i'm sorry but we are out of time. we have a hard stop at 930 time it. i would like to thank both senator conrad and senator greg. in a town where we're used to, watching people, shouting at each other. we had a pretty intelligent, smart discourse this morning.

9:30 am

and i'd like to remind the audience that both senator conrad and greg are available for speaking. i hope you'll look to them for your meetings that are coming up. there's a saying that there is no free breakfast. this is almost the. building would ask is before you leave there's a short questionnaire. it will not take more than 60 seconds to complete. and if you do it we would really appreciate it. i'd like to again thank our sponsors, broadmoor, bdo and ceo updates, and, of course, our partner, the u.s. chamber of commerce. thanks so much. have a great day. [applause] ♪ [inaudible conversations]

9:31 am

>> we will have more live coverage this afternoon here on c-span2. at 1:00 eastern the national immigration forum will host a discussion examining ways to reform the u.s. immigration laws. speakers include u.s. chamber of commerce president thomas donohue, citigroup vice-chairman, and also indiana's attorney general greg reseller. that is live at 1 p.m. eastern here on c-span2. we are coming set of live events on.

9:32 am

at 1230 time that eastern vice president joe biden speaks at the conference of mayors winter meeting. live coverage on c-span again starting at 630 eastern. >> he had been talking about this dream that he had. he talks about it for years, the american dream and then it becomes his dream and he had been in detroit just a few months before. he talked about i have a dream. america will someday realize these principles in the declaration of independence. so i think he was just inspired by that moment. >> sunday on after words, clayborne carson recalls his journey as a civil rights activist, participate in the

9:33 am

1963 march on washington to prominent historian and editor of martin luther king, jr.'s papers. it's part of three days of the booktv this weekend. >> next, secret and exchange commission chair dan gallagher shares his ideas for reforming the dodd-frank financial regulation law. also talks about the commission's 2013 agenda. mr. gallagher was asked of the securities and exchange commission commissioner, appointed by president obama and took office in 2011. this was hosted by the u.s. chamber of commerce but it is just under an hour. >> good afternoon. thank you for joining us. i'm david hirschmann, president and ceo of capital markets

9:34 am

compared is here at the u.s. chamber of commerce. our work was one over six years ago before the financial crisis because at the time on a bipartisan basis a group of folks that we had commissioned together told us that the financial regulatory structure served his country well for 75 years was no longer working. that it was out of date, that they were too many gaps, too many layers, and that somebody should get around doing financial regulatory reform before the next crisis. and shortly thereafter, a crisis did, in fact, happen. and the need for financial regulatory reform became even clear to the american people. i wish i could tell you that dodd-frank had achieved everything certainly we hope we reform, and certainly it did some of the things that needed to be done. but despite having over 400 required regulations across 21 regulators, pop quiz anybody who can name the 21 agencies in

9:35 am

charge, it did nothing to reduce the complexity or to really fundamentally modernize the structure. in some areas it simply fell short but in other areas it didn't act at all. so now that we are two years into it, we will propose shortly in february what we are calling are fixed and replace agenda. areas of dodd-frank that need to be fixed because they're not working. areas that needed to be added because they were not properly dealt with. it's important to remember that when congress first that with financial regulatory reform 75 years ago they didn't do it in one bill. they have several considerations to get right, and finally areas that need to be replaced just because they can't be made to work, no matter how laudable. why do we do this? we do this because financial regulation impacts the way every american company, whether small medium or large company, whether

9:36 am

you're a startup our amateur from, whether you are private or public, whether you're republican -- public and indigo private, or public intend to go private. whether you're growing are trying to turn around the firm, use a need and access capital. whether you're a small company trying to max out a credit card to buy the first piece of equipment or hire the first employee, or a larger company trying to launch a product, a new product to go to a new market. you depend on financial regulation to be right and to have a little plainfield. in fact, every way that companies of very size and shape use of financial services industry is impacted by dodd-frank. talk about the needs of capital whether public or private, credit and access to credit. that's why the work of the consumer bureau and the volcker rule are so important to the way companies manage risk and the ability of nonfinancial firms to manage their financial risks, whether interest rates are

9:37 am

currently, so-called derivatives market, and cash flow liquidity, and confront the fundamental role that money markets play to help many companies manage their day-to-day liquidity. all these things are happening at the same time. and the changes are significant, and it's important we get right. this is not a question of whether financial reform should be more or less. it should be, we call the right way or wrongly. how do we make sure that we get it right? for is, it's to preserve the perverse sources of capital the drive job creation and the american economy. today we will hear from sec commissioner dan gallagher who i think is a well-positioned to lay out an agenda for this in the next year, and we hope that this is an agenda that historically which has attracted bipartisan support, can do that again. sec commissioner gallagher brings a unique combination of

9:38 am

background. first he started off his career in the real world as a general counsel for a financial services firm. then joined the staff of commission of paul atkinson also worked with commissioner. worked for, at the sec as deputy director and acting director one of the largest divisions, the division of trading markets. has been on the senior professional staff of the sec and then was in private practice, and then about 14 months ago was confirmed by the u.s. senate as the next security and exchange commission. i think everybody knows him will tell you three things about him first, he is subsequently smart. he understands the complex issues. second, then he is, has an ability to see another person's perspective, and really make forward progress on issues and understands that you can achieve consensus while still remaining true to principle. and, finally, that he is a great person to work with and he is

9:39 am

somebody -- so for those reasons and many more we are delighted that sec commissioner dan gallagher here today as our keynote speaker. dan. [applause] >> thank you, david, for that kind intro. it was just 14 months ago that i started and 40 month ago since i gave my first speech here in this building. it seems like yesterday, but i think that speech shows how important it is her sec commissioners to get out and about. so i'm pleased to be here this afternoon addressing such strong supporters of american global leadership in capital formation, which is of course one of the foremost goals at the commission. and before i continue, as you all know i must tell you my remarks today are my own, and do not necessary to represent the views of the commission or fellow commissioners. and you're about to find out w

9:40 am

why. [laughter] as i'm sure you're all aware, next monday the nation will observe both the inauguration and martin luther king, jr.'s birthday. what you may not be aware of is that monday also is that money also worked for two and a half year anniversary of the enactment of the dodd-frank act. to commemorate the occasion, i'd like to take a few moments today to talk about the act. specifically, the misallocation of resources and opportunity costs that have arisen from the many false assumptions underlying the act and how they continue to impact the commission's everyday efforts to carry out its mission to protect investors, maintain fair, orderly, and efficient markets, and to facilitate capital formation to you can say this about the dodd-frank act. it's a perfect example of not letting a good crisis go to waste. indeed, the act is a model of the new paradigm of legislation, a core concept, in this case

9:41 am

regulatory reform, overwhelmed by a grab bag of wish list ite items. what continues to amaze me about the act is not only what it covers in its 2319 pages, but also the crucial regulatory issues it does not address. the juxtaposition of the two is quite frankly jarring. act tasks that sec with a mandate to create unprecedented new disclosure rules relating to conflict minerals from the congo. but not to reform money market mutual funds which, we were later told, are ticking time bombs with systemic risk. dodd-frank addresses extracted resource payments made by u.s. listed oil, gas, and mining companies. but leaves the reform of freddie mac and fannie mae for another day. the act fundamentally restructures the nation's financial regulatory infrastructure by establishing the financial stability oversight council, not to

9:42 am

mention the consumer financial protection bureau, but failed to eliminate the redundancy of having the sec and the cftc share jurisdiction over substantially similar and interrelated products and markets. dodd-frank creates a system of regulation for so-called cities, or sci-fi's for some in the crowd. but does not address the shortcomings of the short term funding model of banks that continue to be too big to fail. the dodd-frank acts attempt to solve the financial crisis illustrates the peril of false narratives. justifies the mandate as answers but only after asking the wrong question. i suppose this shouldn't be a surprise given that the statute is not the product of a bipartisan compromise that was enacted surely after the onset of the crisis, many months before the bodies -- issued their reports. this was a markedly different

9:43 am

approach than the deliberative process undertaken after the 1929 stock market crash. in total, the dodd-frank act contained approximately 400 specific mandates to be implemented by agency rulemaking, with approximately 100 of those falling on the sec. as he has adopted final rules implementing nearly a third of the statutory mandates and continue to devote tremendous amounts of resources to drafting additional proposals, completing the required studies, and implementing the new rules. the result has been a dramatic increase in both the volume and pace of sec rulemaking. as i've said in the past, it's no exaggeration to say that the commission is handling 10 times its normal rule-making volume, with normal being the post-sarbanes-oxley level of activity, itself a marked increase from the pace before that law's enactment. as a result, the sec, like other regulators, is now being with

9:44 am

the problem of rushed, inadequate rule proposals that were pushed out in a bid to meet arbitrary congressional deadlines. as you might expect, it isn't easy to promulgate high quality final rules from faulty proposals. the volcker rule serves as a case in point. this increased pace raises two sets of concerns. the first stems from the difference between getting rules done and getting them right. smart regulation requires taking the time to understand the problem that needs to be addressed, including not only the proximate cause of the problem but also the often complex and hidden factors underlying that problem. it's at this stage whether peril of false narratives is at its greatest, for incorrectly identifying the causes of a problem, whether outright or by oversimplifying compensated issues, makes finding the right solution for more difficult, if not impossible. and it should go without saying

9:45 am

that we need to ensure that we are performing a rigorous cost-benefit analysis of all rules, whether proposed or fin final. the second set of concerns centers around the concept of opportunity cost and the misallocation of limited resources. i have no doubt that the businesses represented by the chamber understand the concept of limited resources and the need to set clear and sensible priorities far better than does the federal government. every hour spent by the sec staff on drafting rules or carrying out studies to at the dodd-frank mandates represents one less staff hour spent focusing on the commissions core regulatory responsibilities. ..

9:46 am

>> such as hedge b funds or private equity funds. the rule identifies certain specified, permitted activities including underwriting, market making and trading and certain government obligations that are accepted from these prohibitions but also establishes limitations on those accepted activities. the legislative text of the volcker rule defines in expansive terms key concepts such as proprietary trading and trading account and grants the federal reserve board, the fdic, the occ, the sec and the cftc -- there's a few of them, david -- the rulemaking authority to further add to those definitions. the banking agencies and the sec

9:47 am

issued a proposal in october 2011, weeks before i started as a commissioner i'll point out, with the cftc following in february of last year. fifteen months later, the rulemaking remains at the proposal stage with ongoing talks between the agencies aiming to address the myriad concerns raised in over 18,000 comment letters regarding the dire, albeit presumably unintended consequences, they argue, would result from the proposed implementing regulations. and yet, and i quote, if you look at the crisis, most of the losses that were material for the weak institutions and the strong, relative to capital, didn't come from those proprietary trading activities. they cam overwhelmingly from what i think you can describe as classic extensions of credit. those aren't my words. treasury secretary geithner spoke them this september 2009. -- in september 2009.

9:48 am

in case secretary geithner merely misspoke, i'll provide another quote from a different speaker, this time from march 2010. proprietary trading in commercial banks was there but not central to the financial crisis. that speaker, paul volcker. p don't get me wrong, as illustrated by notable hedging failures last year, bank trading and hedging practices can, indeed, be a whale of a problem. it's not a problem the volcker rule or the dodd-frank act as a whole purports to address. like much of the act, the volcker rule is a solution in search of a problem. the act, however, is still the law of the land, and banks have long since accepted the rule and its implications for their business activities. in fact, i've been told by several firms that although the implementing rules have yet to be finalized, they've taken significant steps to shut down their u.s. prop trading activities and in some cases have already done so completely.

9:49 am

even as firms have looked to the statutory text and spirit of the rule and proactively taken action to bring their hedging and trading practices into compliance, however, high-level staff from five regulatory agencies continue to work behind closed doors to refine a rulemaking proposal that, according to a letter sent to the agencies by a bipartisan group of six senators, quote: has drafted could adversely affect main street businesses by reducing market liquidity and increasing the cost of capital. in another comment letter, senators merkley and levin wrote. the volcker rule demands wall street change its culture. implemented in a smart, vigorous way, the volcker rule can both protect the u.s. economy and taxpayers from some of the gravest risks created by the nation's largest financial institutions while providing plenty of space for these financial institutions to provide the plain vanilla,

9:50 am

low-risk, client-oriented financial services that help the real economy grow. these are certainly laudable goals. almost uniformly, however, critics of the volcker act argue that it is those very plain vanilla, main street, customer-facing products that will be harmed. not necessarily by the text of the volcker rule as set forth in the dodd-frank act, but by the draconian interpretation of the rule that the october 2011 proposed rules would impose upon the financial industry and their customers. notably, our foreign regulatory counterparts in europe, canada and japan have been some of the fiercest critics of the proposed implementing rules. i had the opportunity last week to meet with regulators and industry participants in the u.k. and ireland where i encountered a distinct lack of enthusiasm for either the volcker rule or or its ring-fencing counterpart proposals set forth by the u.k.

9:51 am

independent commission on banking and the e.u.'s likennen group. indeed, sir john vickers, chairman of the independent commission, has already criticized the u.k. coalition government from backing away from his original proposal while the european commission's recent report summarizing the responses received to the likennen report acknowledges the widespread opposition to the proposal in a charmingly understated fashion, stating: in general banks welcome the group's analysis but argue that a compelling case for mandatory separation of trading activities hasn't been made. they felt the proposal wasn't backed by the required evidence and that there was a need for a thorough impact assessment. with all due respect to my friends in the european financial regulatory community, when a regulatory proposal is viewed within the e.u. as being too harsh on a financial industry and harmful to markets, i think it's a clear sign that

9:52 am

it's time to take a step back and reevaluate. regardless of what happens with respect to the vickers or likennen proposals, even if all of the most vitriolic allegations wall street's harshest critics set forth are true, even if our financial giants act solely and ruthlessly out of craven self-interests, those financial institutions know that the volcker rule is not going away. as such, they've already begun the process of determining which of their activities will be prohibited under the rule as set forth in the text of the dodd-frank act and proactively moving to shut down their truly proprietary trading desks as appropriate. accordingly, as my friend and i have often stated, the final regulations implementing the volcker rule should, for the most part, simply be a codification of what most banks have already done in response to the requirements set forth in the legislative text.

9:53 am

the critic of the proposing release are no longer, if they ever did, realistically contemplating repeal of the volcker rule. they simply want us to get the implementing regulations right. the october 2011 proposal fails to accomplish this goal by focusing only on the latter part of senators merkley and levin's call for implementation of the act in a smart, vigorous way. operating on the narrative that banks' proprietary trading practices were a central cause of the crisis, the proposal eshoos a focus on smart regulation in favor of pursuing the most vigorous interpretation of the rule's mandates. the proposal throws the baby out with the bath water, along with the rub bear ducky -- rubber ducky and all of the plumbing for good measure. [laughter] just making sure you're awake. rather than carefully examining banks' trading practices to determine which of those

9:54 am

practices constitute proprietary trading and which are instead customer-facing activities providing liquidity and reducing the costs of capital, it stretches its definitions of covered activity on an almost punitive basis as if based on an assumption that any trading that could result in profits for the trading entity must fall within the ambit of the volcker rule's prohibitions. this failure to separate market-critical, customer-facing activities from true proprietary trading illustrates the second set of concerns; opportunity costs and the misallocation of resources. the entire rulemaking exercise so far has been carried out in a manner that has wasted the resources of all the agencies involved. by every account the bank regulators have taken the lead role throughout the rulemaking process, presumably this stems from the fact that the rule applies to the vast financial firms regulated at the bank holding company level by the

9:55 am

bank regulators, coupled with the by zahn teen nature of interagency rule making and as well as the washington power game. the volcker rule, however, isn't about the financial entities involved or the relative political standing of the different regulatory agencies, but instead the activities in which those entities engage. those activities, the trading and hedging practices of those entities, unquestionably fall within the core competencies of the sec can. for example, the sec has built an extensive library of rulemaking and interpretive releases concerning exceptions for bona fide hedging or market making in the context of short sales. those exceptions which date back to the early 1980s built upon the bona fide hedging exceptions to the commission's proprietary trading rules for members of national security exchanges set forth in a 1979 rulemaking, the rule expressly envisionses that quintessential market activity

9:56 am

continue to be carried out by the firms affected by the volcker rule. yet the agency that has regulated securities market making in order to facilitate liquidity and promote the efficient allocation of capital for decades has played a secondary role in drafting regulations to implement this rule. and all of this comes with a cost. both the commission staff playing second fiddle and the banking regulators struggling to convert the widely-lambasted proposal release into workable legislation could be focusing on other matters rather than spinning their wheels with no end in sight. simply put, we could be spending our time in a far more productive manner. focusing on mandates that are critically important such as those in the jobs act as well as addressing the sec's basic blocking and tackling. indeed, one personal frustration of mine has been the commission's inability to fully implement what i believe is the most useful and important provision of the dodd-frank act, section 939a mandate to remove

9:57 am

all references to commission-registered credit rating agencies formerly refer today as nationally-recognized statistical rating organizations from all agency regulations. this clear and direct mandate is actually responsive to one of the core problems underlying the financial crisis. that was overreliance on inaccurate credit ratings by both investors and regulators. yet the most important rules continue to include such references. meanwhile, fsoc -- charged with averting the next financial crisis -- is apparently spending more time hectoring the commission, a purportedly independent agency, on the reform of money market funds, an issue that falls directly and solely within the commission's sphere of responsibility but that was somehow not important enough to be addressed in the dodd-frank act than they are focusing on the bubbles that have the potential to cause another crisis.

9:58 am

on the issue of money market funds, i'm happy to report that craig lewis and his fine staff in our economic analysis division have completed the rigorous study and economic analysis that a bipartisan majority of commissioners had long ago asked for in advance of considering a new rulemaking. we are currently working with the economic analysis staff and the division of investment management to shape a reform proposal based on that rigorous economic analysis. and separately, i'm encouraged by chairman walters' commitment even as we continue to implement the mandates to focusing as well on the everyday, core blocking and tackling issues that affect investors most. in the coming monthings, i look forward to would being together to crease the commission's -- to address the commission's priorities such as the long overdue amendments to the net capital and customer protection

9:59 am

rules and longerrer-term ones such as engaging in a formal, thorough evaluation of equity market structure issues last done in a comprehensive manner in the commission's market 2000 report always way back in 1994. for all the recent talk of gridlock and a divided commission, i believe that notwithstanding our party and policy differences this commission is fully united in its desire to carry out the commission's mandate to protect investors, maintain fair, orderly and efficient markets and facilitate capital formation. with a clear data and analysis-based understanding of the problems we face and a complexity of their underlying cause cans coupled with the deliberate, measured allocation of our resources, i believe that the commission can accomplish great things and can avoid the mistakes of the past over the course of the coming year. i thank you all for your attention as well as for your commitment to advancing our

10:00 am

nation's global leadership and capital formation by supporting capital markets that are most, that are the most fair, efficient and innovative in the world. i'd be happy to take any questions you might have. [applause] >> commissioner gallagher, that was excellent remarks, and i appreciate your willingnesses to take some questions. i would just ask if you have a question, raise your hand. we will bring a microphone to you so that your question can be answered. just wait until the mic comes to you. and while the first question comes, let me start with a question on one of the topics you covered which is money funds. um, you clearly laid out that there is a strong consensus among the commission to do things that would strengthen the product without destroying a product that from our perspective fundamentally is fundamentally important to a large segment of american

10:01 am

business. in fact, the fsoc in etc. proposal kind of -- in its proposal kind of has, you know, they clearly state the importance of money funds and say that they want to preserve the product, and then they lay out a thurm of ways to kill it -- a number of ways to kill it. we are, i think, all hopeful that the sec will be able to reassert its jurisdiction here, and you've indicated that among the things you are willing to at least consider would be a floating net asset value. but there are enormous complexities in implementing a floating asset value such as the tax accounting and operational challenge. could you say a little bit more about what your thinking is in that area? >> yeah. now that i have a voice again with some water, i've had a little jet lag and a cold. it can't hold me back. so, yes, i think that money market funds will be one of the primary issues that the commission tackles in the coming months. you know, the fsoc process is, obviously, underway, but quite

10:02 am

frankly i think we at the commission can and have been proceeding without too much reference to what's going on with fsoc. and i think that there's sort of a new spirit at the commission working with the staff, working with industry and working amongst the commissioners in a consensus that we need to take some action. obviously, been a lot of press lately about potentials involving the floating -- i've expressed my view that i think that would be a great avenue to explore recognizing, david, as you point out that there are pretty serious tax and accounting issues that need to be addressed and haven't been addressed despite the fact that this proposal has been lorded about the industry now for four or five years. so on the accounting front, um, i'm hopeful that as the commission has plenary authority over accounting standards of the united states we can actually figure something out there. if we can't, then we're all in much more serious trouble than i thought. and on the tax side, obviously,

10:03 am

with fsoc's interest in this issue and the treasury secretary being the head of the fsoc and irs within treasury, i think that i would hope and expect there, too, that we can find ways to mitigate if not to fully resolve the issues. on the operational side, obviously, that's just something we have to work with the industry. i think that's something we can learn a lot about through a notice and comment process. and i think it's something we'll take very seriously. but i'm encouraged to see that over time, you know, we've gotten the engagement from industry, we've heard discussion. certain ideas i give schwab in particular credit for the op-ed they ran in the journal talking about a path forward that i think makes a lot of sense if we ended up there. so we'll, hopefully, soon here see a proposal come out of the commission, something that's more tailored that'll engender. much more cooperation from the industry than we've seen before. and, you know, when you put together a proposal as we had last year that some called it

10:04 am

death by hanging, death by shooting, it's ease -- easy to see why you don't get that level of cooperation and have these breakthroughs like we've been having recently. >> questions from the audience. right here. if you could just introduce yourself. >> yes, john -- [inaudible] competitive enterprise institute. thank you so much for speaking to us today. my question's about, touches on the money market rule but more on the fsoc's authority itself. where exactly does the financial stability oversight council's authority begin and end, i mean, over this rule and other things that the sec deals with? can it just, you know, come in and intervene anytime it doesn't like what the sec does or doesn't do? >> well, it's a great question, john. you know, not being a member of the fsoc personally, i can't tell you i know anything from behind closed doors. the statute, title i of

10:05 am

dodd-frank in establishing fsoc made clear that its members are the heads of the constituent agencies. so the chairman of the sec is a member of fsoc, the rest of the commission is not which i believe personally to be an issue in and of itself. so as to the legal authority in title i, you know, my understanding loosely is that they need to when they identify systemic risk take certain actions. in this case they've taken what they call the 120 route which is to put out a proposal when the primary agency responsible for the matter hasn't done so. and then when they get their comments back and decide which route they want to take, they can send it back to the primary agency, in this case the sec, telling them to do as instructed, to take an alternative or to do nothing but explain ourselves. so i'm hoping we just never get to that stage on money market funds. but it, your question raises a

10:06 am

much larger issue which i think i just alluded to in the speech about the independence of the constituent members, especially the so-called independent agencies. and, you know, how independent are you if fsoc can drive your policy. money market funds, you know, because they did have a role in the crisis with the breaking of the buck of the primary fund, reserve fund, obviously, it speaks more to systemic issues than ore things. i -- other things. but if you go and look to the fsoc annual report, you'll see other things including high frequency trading, etfs and others which i believe to be much more germane to the sec and not to systemic issues. and so where it begins and where it ends, i don't know. >> other questions? right here. >> jim angel from georgetown and wharton. you mentioned the fact that the

10:07 am

sec's behind with the jobs act rules. and as you know that many businesses cannot raise capital until those rules are actually issued. what problems would there be if the sec issued some temporary, principles-based rules that would be simple enough that it would allow people to start raising capital in this environment while meanwhile it gives you experience and time to get them right? >> well, i think -- good to see you, professor. i think that question goes specifically to the larger question of the problem with principles-based rules which, obviously, at the sec we're not used to. we're very prescriptive in our rulemaking. but i'll point out to you, though, too when we try if you look at the proposal on general solicitation, when things are a little more principles-based and flexible what we get back from industry, from lawyers, from, you know, trade groups is, please, give us a safe harbor with three easy steps and a checklist so that we can insure

10:08 am

ourselves against liability both from the sec and civilly. and so there is oftentimes a press to get that sort of prescriptive rulemaking. so i just, quite frankly, i'm skeptical it would work because i don't know if folks would take the ball and run with it if there was, you know, a principles-based approach here. i think instead the sec, we -- the commission -- need to just get on it and get the rules proposed and finalized. the fact that general solicitation's not done is a travesty. you know, the deadline was in july of last year for final rules. and we only got a proposal out at the end of august. so i hope and expect that there's a pathway forward. it'll depend on which way chairman walter wants to go. >> right here. >> [inaudible] um, i'm wondering whether you could comment on whether you'd be supportive of --

10:09 am

[inaudible] volcker rule given the amount of time -- [inaudible] >> i've publicly stated, you know, for the last nine, ten months that i think we need to repropose the volcker rule. you know, i think at the end of the day it's a legal analysis under the apa. whether a proposal that was as vague as the volcker proposal was that generated 18,000 rather substantive comment letters is actually actionable for purposes of a final rule. and so that said, i can be a practical guy if the final rule made sense and was clear, and the legal analysis showed we could go final, then i think we should. but i don't think that we should be at the sec left behind by the bank regulators. i don't think we should front run them either. but, you know, i think our role

10:10 am

in this process is critically important, seeing as most of the activity we're talking about on the trading side should be happening on the broker/dealer sub of these institutions. we'll see what the staff can come up with, what makes sense, and then we'll just see if we can move forward. >> right there. >> good afternoon. john -- [inaudible] from dreyfuss. on the issue of the removal of credit rating references in 287, that was originally proposed as a separate release before -- >> right. >> -- the money market reform got so big. since then it kind of has become tied with money market reform, you know? the next release will address, also, the credit rating. do you still foresee that as something that must be done together? can it be something that, you know, should be done separately maybe, you know? is the issue removal of the rating references contingent or not contingent on whether you go

10:11 am

to a floating nab? do you have any comments on that? >> i don't have a strong personal preference about how it comes. i'd like to see it, vote on it and get it done with. you know, the preference of former chairmen, the staff to couple it up with money market fund reform, larger money market fund reform is irrelevant to me. i think that we need to carry forward, you know, and simply get it done. 28715c31 which is broker/dealer capital rule, those are the two big rules till on our books with rating agency references in it, and of all the mandates in dodd-frank, i think this one hits the core cause of the financial crisis, right? the failures of the rating agencies and the overreliance on the ratings. and yet despite that, you know, we have conflict mineral disposal, but we don't have removal of those references. i just don't get it. >> [inaudible] >> i don't know. you know, i haven't seen the proposal yet.

10:12 am

i doubt it, and i don't think i would push for it if it was going to slow down the larger money market fund reform. again, that was just a preference last year. but i do hope regardless that it comes soon. >> you know, a lot has been made about the slow pace at which the jobs act has been implemented. in some ways, you know, it's even slower than that because many of the ideas in the jobs act, the best ideas were ideas that the sec had gathered and considered and said it was going to adopt for years before congress acted. >> right. >> and then, you know, one of our concerns is that there is, you know, the jobs act, today-frank's the most difficult two-thirds of dodd-frank and other areas, there's a whole pent-up area where i think you could achieve pretty broad bipartisan consensus. and yet the sec's agenda always seems to be subsumed by other issues. you mentioned some, conflict minerals and others. those cases were mandated.

10:13 am

but if you go back to the whole proxy access debate or perhaps the future debate coming on political disclosure, good, bad or indifferent, those are highly polemic issues that have consumed massive amounts of staff and commissioner time at the expense of a whole number of other things. what path forward do you see over the next year, and what's your personal view on the political disclosure proposal? >> yeah. i agree with your statement. i think that there's been a lot of distraction. i've spoken publicly about the fact that we've been sort of led astray by, as you point out, highly politically-charged issues. we're supposed to be a bipartisan, essentially apolitical agency. but clearly in setting the agenda, political preferences have been made. and so i disagree with them. there are things, many mandate cans -- it shocks people, we're a third of the way through the dodd-of frank final rules,

10:14 am

right? everybody thinks dodd-frank is done, wall street's been reined in, july 2010. hasn't happened. a third of the way through, we'll be doing this for years unless congress changes something. and so, you know, it really is incredibly important for the agency to get the priorities straight, to focus on what's important within the dodd-frank mandates, within the jobs act mandates which pretty much to me are all of them, and then, of course, to look at these core blocking and tackling issues that i keep talking about. mundane things that will never get you a new york times headline. transfer agency regulation, broke orer/dealer net capital rules. these are important things. this is what the agency's all about, and they protect investors. so i have great confidence, though, as i said earlier that chairman walter understands these issues and will get us, i think, on a pretty good path towards focusing on the right priorities. as to political campaign disclosure, that should not be one of our priorities. that is just a, you know, a

10:15 am

political wish list item. obviously, the recent promulgation of the reg flex agenda showing it as an agenda item, i think, is unfortunate. but i can speak for myself, i think i can speak for commissioner pray days too, we have no interest in pursuing that, and i think that should give you at least temporary comfort. >> other questions. yep, right here. microphone coming to you, if you'll just wait one second. >> thank you. neil roland. commissioner, both you and chairman walter have been proponents of municipal bond reform. um, where do you see municipal bond adviser rule headed and other aspects of municipal bond regulation? >> yeah. you know, i've agreed with elise since i walked in the door and, obviously, for years before that that we need to focus a little more attention on the muni

10:16 am

space. all sorts of issues, many of which were raised in the commission's report that came out last summer. where that's going to go agenda wise, i'm not exactly sure yet. i think that taking a step back we actually have to focus very intently on the fixed income markets generally. it amazes people, i was co-acting director of trading and markets in 2009. we had two people focusing on the fixed income markets, and they both were on the muni side. there aren't full-time employees that come into the commission every day and think about fixed income markets generally. and we have, you know, 110 focusing on equity markets. there's a fascination with micro equity market structure issues. and it's borne out by the fact that now we talk about writing rules about microseconds, right? that'll instantly be stale the minute we get them into the federal register. so i think a focus on fixed income especially in a 0% interest rate environment, right, where we're watching

10:17 am

investors chase yield in crazy places where they don't want to be either, right? they'd rather be in an interest-bearing cd, but they can't be, so they're in the junk bonds and munis. it's great for the corporations financing themselves, but where's it going and what's going to happen when interest rates go up and there's an exodus in those markets, in particular for the small investors who don't have the dealing power of the big asset managers and others in the space. so this is a big issue, right? if i was on sock, this is what -- fsoc, this is what i'd be focusing on instead of etfs, but i'm not. so, but i do think because of elise's interests, the commission's interests generally -- i don't think it's just the two of us -- that you'll see a focus on fixed income issues generally, and i think that'll be a very positive thing for the agency. >> yep. question. >> john -- [inaudible] from the bond buyer. follow up on that question. i'm a reporter also.

10:18 am

what about the sec's report that came out a few months ago and whether or not the sec will start to seek the authority over issuers of municipal bonds? >> yeah. i mean, obviously, the report was careful not to seek the authority and rethink the tower amendment. i think there's so much that can be done outside of that that we should focus on the possible instead of the perfect. and so, again, i just don't know exactly what product will come out, and i think there probably would be the potential for several interpretive releases, you know, further round tables on issues and, i guess, potential rulemaking where possible whether through msrb on muni issues. one thing, neil, i forgot to respond on the muni adviser piece specifically. i wouldn't put it as, you know, a huge priority, you know, in the con b text of responding to the financial crisis.

10:19 am

i wouldn't put this high on the list. however, i do think we owe clarity to the markets, and we should prioritize that because it's been hanging out there way too long. so i do think it would be a relatively high priority agenda item for the commission this year. i think there's somebody over -- >> let me take you back up to the 30,000-foot level one second. you know, i think if you survey the american people, you know, there's somehow this perception that all financial services forums are based within three square blocks in new york and maybe that there's just a small number of firms. as you travel the country, you realize that the financial services industry is incredibly diverse. and in our view, at least, that has been a source of strength which is that job creators of every type and size have been able to go to the right kind of financial firm -- small, medium-sized or large -- whether

10:20 am

it's a bank or nonbank, whether it's an asset manager or otherwise to get the financing and the liquidity and the risk management and all the other ways that they depend on financial firms they need. i don't think that story is well enough understood, and the danger in implementing 400 rules is that you'll begin picking winners and losers among financial firms that you will reduce the choices available and end up not be by one single rule, but by the combination of all of them suffocating the way that american entrepreneurs access financial services. what's your views on that? >> i think you touched a chord that i've been talking a lot about lately in less formal settings. but to me, the issue is capital markets versus the banking markets. and what i fear coming out of the crisis what you see in dodd-frank, what you see in the e.u. directives and international bodies like fsb here, fsoc domestically is sort

10:21 am

of the bank regulatory view of the world taking over the capital markets, right? the notion of derisking in safety and soundness. it sounds great when you come out of the crisis, when you, you know, have seen hell and come back. the last thing you want to do is engage in risk taking or encourage risk taking as a regulator to allow it to happen at all because you got burned in whatever narrative about the crisis. but as you know, the capital markets are all about risk. without risk we don't have the capital markets. you have to put your capital at risk if you want to get a return. and we can't derisk them, right? money market funds is a pretty good example when you start talking about silly things like capital buffer, derisking something at 50 basis points that might kill the product, right? at the racing of -- at the risk of killing the product. this is the mindset that's pervading. it's something we all have to watch because soon enough, you know, if there aren't enough

10:22 am

opportunities to take risk and get a return, the economy is bad enough now. let's, you know, see how it does after that mindset takes over. >> thank you, david. thank you, mr. commissioner, for coming today. um, you've -- thanks for your remarks. obviously, this is a global economy and financial services especially, um, it's important to look at it from a global perspective. and it was very useful, i think, for you to remind us of the comments that europeans, especially the japanese had on the volcker rule. but with respect to money markets, mutual funds, there's talk of european action here in the near future. so i was wondering if you have any advice to our friends across the ocean as far as action or what not with respect to what the sec might be thinking of doing? >> well, thank you, many commissioner, for your question -- mr. commissioner, for your question. i, yeah.

10:23 am

i, you know, was in london and dublin, and i don't know which jurisdiction was more interested in the money market fund debate. obviously, it's a big industry in both of those locales. and, you know, they, um, in both places i was told by industry as well as high-level government officials that the ec is on the cusp of releasing consultation paper on money market funds, and they're doing so because they view the sec to be on the sideline. that everyone had wanted the sec to take the lead, but that after the famous events of last august that we were on the sideline and never coming back. so i was happy to be able to share with these folks, which was a limited pool, no, we're actually working, and i hope and expect within the first quarter here to have a proposal out for comment, which was a great relief to some but unen known to far too many -- unknown to far too many. so if the international community was waiting and

10:24 am

watching the sec and that was the preference just like fsoc says it's the preference for the sec to take action and not them, well, they should continue to watch and wait. because soon enough we'll have something. it'll be tailored, i think, to the problems that were experienced in 2008 as borne out by the staff study that we ordered that's up on the web site. you know, for the first time you have an sec narrative of the problem out there for the industry and other regulators to react to, to challenge, to agree with in parts. and, therefore, i think it's going to make it a much better rulemaking. so i would hope and expect, obviously, the ec's free to do whatever it wants, but given the fact that we have 2.7 trillion in this market, it's a macroeconomic issue for us that they would want to wait and see what we do first. >> in the back. >> hi, i'm mark shep with

10:25 am

investment news. i'm wondering what is the timetable for a request for information for a cost benefit analysis of a potential fiduciary duty rule for retail invest, advice, and how do you see that issue developing this year? i realize it's not a mandated dodd-frank rule. does that mean it's going to continue to languish? >> it can't languish if it's not mandated. [laughter] so i call it the deliberative process. the proposal the staff has worked on to, you know, bring in economic data for our analysis is pretty well put together. i think there's some language issues we're working our way through. i think at the end of the day, you know, we have a new chairman here. she's trying to figure out which priorities to focus on, and, you know, i think this would be an easy one to prioritize if she

10:26 am

wanted to because it's further down the road than others. that said -- and i've said this in speeches -- it's not mandated. we should be very deliberative, and i'm not convinced we should do anything in this space under our 913 authority. this proposal, this request for comment we're putting out is simply to figure out should we do anything. and if we do anything, do we have the right analysis undergirding it. and so, you know, as things go at the commission these day cans, as important as this issue is to the industry, it's not the most burning priority. to me. >> let me ask one final question about a lot has been made about cost benefit analysis and the need for regulators, particularly the sec but certainly all regulators, to do a cost analysis of the regulations they're imposing and understand the benefits.

10:27 am

and many people think of that as kind of doing a check the box economic study after you decided what you're going to do. >> right. >> and our frustration, i think, has been that really what it requires, what regulators should do is define the problem they're seeking to solve, look at the range of options that would actually solve that problem, and then find the most cost efficient. so it's not a question of the cost of regulation, it's about how best to achieve a desired objective. and ultimately, there's an obligation by all regulators to do that. i think too often the sec in particular but many regulators have simply kind of viewed it as a compliance effort rather than a driver of smart rulemaking. >> right. no, i -- it wasn't a question, but i'll respond to it, david. [laughter] i agree with your statement, and i, you know, on this front will give great credit to former chairman shapiro on almost a

10:28 am

year ago mandating that the staff put together what we call the economic analysis guidance that's up on our web site that was made public last year that binds the commission staff in our rulemaking process as to how they're supposed to engage the economists, look at data, look at options and turns, explain the decision-making process. commissioner or pray discuss says it better than anyone, at the end of the day it shouldn't be about this complicated process, it's just proving out your work, right? a lot of times the staff did do work, they just didn't explain the choices they'd made, they didn't explain the data and other things they'd taken into account. so this new paradigm mandates that they do it. and it holds us accountable. you know, and i think it's a new day for the agency. obviously, there are things in there i could quibble with. it was a nonnegotiated document. i think this notion of, you know, mandatory versus discretionary as i mentioned in my dissents on conflict minerals

10:29 am

and extractive resources don't make a lot of sense. but putting that aside, i think it is a new day. i think that the role of the economists has been totally changed in the agency. they're not the post facto checklist guys that they used to be. and so i'm hoping or for those reasons that we simply just have better rules and not longer ones, but better. and i think we've seen some change in that regard and hope any throughout this year as we work to folk off these important priorities that this new paradigm carries forward and folks like you don't have to sue us as much. >> well, we don't like suing either. [laughter] it's expensive, and we always believe with all due deference to the lawyers in the room, it's expensive. >> absolutely. >> and second, ultimately what we're trying to achieve is to make sure that, you know, you always get a better outcome through the deliberative process as a regulator than you do in the courts. >> and i'll point out in that regard, i already mentioned the

10:30 am

staff study that went out on money market funds. it is revolutionary in so many ways, dade. i mean, it is untouched by the policymakers. i'll confess i didn't even read it before it went up on the web site. we put it up there, there's an appendix i can't even read because it's in math. you know, it is, you know, us putting our ph.d. economists up against the industry's ph economists, let's come hash it out. you know, they relish this stuff internally. but it's a new day too. again, because we've put out there the baseline that we're thinking about as we move forward on rulemaking, allowing folks to come in and challenge it to make sure that we got the narrative right, that we don't regulate based on false narratives as i talked about before with dodd-of frank. >> one of the first lessons i taught my daughter was look both ways before you cross the street, and when you don't do the kind of study that's now been done on money funds and, certainly, we don't agree with everything in there, uni, it's literally like crossing the

10:31 am